热门资讯> 正文

内幕报告:随着新领导层的出现,盈利季节开始

2026-01-20 04:24

Market Overview

It was another week of choppy market activity. Only the Russell 2000 fared well, as it surged to a new all-time high again. The large cap indices weren't as strong, however. The Nasdaq closed down 0.66%, the S&P 500 closed down 0.38%, and the Dow Jones Industrial Average closed down 0.29%. Tech is still struggling to find its rhythm, but let's see if earnings season can reawaken it from its slumber. Crypto is still trying to carve out a bottom, while precious metals are looking more and more dangerous at these levels.

Stocks I Like

Digital Ocean Holdings (NYSE:DOCN) – 52% Return Potential

What's Happening

- DigitalOcean Holdings, Inc. (DOCN) is a leading cloud computing platform provider offering simple, scalable, and developer-friendly infrastructure and platform tools, including droplets, managed databases, Kubernetes, serverless functions, AI capabilities, and a marketplace for pre-configured solutions, empowering startups and growing tech companies worldwide, providing investors exposure to the rapidly growing cloud services and AI infrastructure sector with a focus on accessibility, innovation, and democratizing cloud and AI technologies.

- The company showed revenue of $229.63 million in the latest quarter, along with $55.99 million in earnings.

- The valuation in DOCN is mixed. P/E is a bit high at 22.13, while Price-to-Sales is elevated at 6.07. EV to EBITDA is solid coming in at 18.81.

- From a technical standpoint, DOCN recently broke out from an ascending triangle formation. This points to a continuation in the underlying uptrend.

Why It's Happening

- DigitalOcean Holdings Inc. is capitalizing on the AI infrastructure surge with its Gradient AI Agentic Cloud platform, driving explosive growth in Direct AI revenue that more than doubled year-over-year for the fifth straight quarter in Q3 2025. This focus on developer-friendly, cost-effective AI tools positions DigitalOcean to capture share from hyperscalers while serving scaling AI-native enterprises and digital businesses in a market hungry for accessible, high-performance cloud solutions.

- Accelerating revenue trajectory and raised guidance highlight DigitalOcean’s operational strength, with Q3 2025 delivering 16% year-over-year growth and the highest incremental organic ARR in company history. Management’s upward revisions for 2025 and expectations of 18-20% revenue expansion in 2026 reflect sustained momentum from AI workloads and general-purpose cloud adoption, creating a narrative of reliable scaling in a competitive yet high-demand sector.

- Strategic AI partnerships and product innovation enhance DigitalOcean’s ecosystem appeal, including collaborations like the one with Persistent Systems for enterprise AI workloads and ongoing enhancements to its comprehensive agentic cloud. These moves deepen customer retention, attract migrations from larger providers, and support long-term growth by addressing the evolving needs of startups, SMBs, and AI developers in a rapidly digitizing world.

- Path to sustained profitability strengthens DigitalOcean’s investment case, with trailing 12-month adjusted free cash flow margins reaching 21% and improving cost efficiencies across its platform. This financial discipline, combined with a balanced performance across AI and core offerings, positions the company to generate increasing shareholder value as it transitions from high-growth investment to a more mature, cash-generative cloud player.

- Analyst Ratings:

- Barclays: Overweight

- Piper Sandler: Neutral

- Canaccord Genuity: Buy

My Action Plan (52% Return Potential)

- I am bullish on DOCNabove $45.00-$46.00. My upside target is $80.00-82.00.

Peabody Energy (NYSE:BTU) – 26% Return Potential

What's Happening

- Peabody Energy Corporation (BTU) is a leading global coal producer and one of the world’s largest pure-play coal companies, mining and supplying thermal coal for electricity generation and metallurgical coal for steel production, offering investors exposure to the energy and commodities sector with a focus on reliable energy supply, operational efficiency, and international markets including the U.S. and Australia.

- The company printed $1.01 billion in the last quarter, along with $3.23 million in earnings.

- Valuation is solid in BTU. Price-to-Sales is at 1.08 and EV to EBITDA is at 9.27. Book Value is solid at 29.11 as well.

- From a technical perspective, BTU is coiled up nicely within a saucer formation. If and when it clears technical resistance, look out above because this could rip.

Why It's Happening

- Peabody Energy Corporation is benefiting from a tightening Powder River Basin (PRB) coal supply in early 2026, as delayed retirements of several coal-fired power units—extended under Department of Energy emergency orders—have kept demand steadier than anticipated. With much of Peabody’s 2026 output already sold forward at favorable prices, this supply constraint supports near-term revenue visibility and pricing power, positioning the company to generate strong cash flows amid ongoing U.S. energy security needs.

- Robust metallurgical coal exposure enhances Peabody’s growth narrative in higher-margin segments. Strategic acquisitions and operational focus on seaborne met coal, combined with global steel demand resilience, allow Peabody to capture value from premium pricing in export markets, diversifying away from purely thermal-dependent revenue and creating upside as industrial activity rebounds in key regions like Asia.

- Strong operational execution and cost discipline drive Peabody’s profitability resilience. Recent quarters have shown effective fleet management, accelerated longwall starts at key mines like Centurion, and favorable volume/cost adjustments for full-year guidance, reflecting management’s ability to navigate market volatility while maintaining a lean balance sheet with minimal net debt and solid cash reserves.

- Policy and regulatory tailwinds bolster Peabody’s competitive position in domestic markets. Recent U.S. legislation reducing coal royalty rates, streamlining permitting, and providing tax credits for metallurgical coal lowers operating costs and improves long-term viability, particularly in the Powder River Basin and other core assets, aligning with broader efforts to support energy independence and critical mineral supply chains.

- Analyst Ratings:

- UBS: Neutral

- Benchmark: Buy

- Texas Capital Securities: Buy

My Action Plan (26% Return Potential)

- I am bullish on BTU above $28.00-$29.00. My upside target is $46.00-$48.00.

Baidu (NASDAQ:BIDU) – 87% Return Potential

What's Happening

- Baidu, Inc. (BIDU) is a leading Chinese multinational technology company specializing in Internet services and artificial intelligence, best known as the dominant search engine in China (“the Google of China”), while advancing in autonomous driving through Apollo, AI cloud services, smart devices, and generative AI initiatives, offering investors exposure to the rapidly growing AI, autonomous mobility, and digital ecosystem sector with a focus on innovation, full-stack AI capabilities, and expansive Internet foundation.

- The company reported $31.17 billion in revenue last quarter along with $3.77 billion in earnings.

- Valuation is very solid in BIDU. P/E is at 13.63, Price-to-Sales is at 2.77, and EV to EBITDA is at 9.36.

- From a charting perspective, BIDU is on the verge of completing a breakout from a saucer formation. This will set it up for a massive acceleration of upside momentum.

Why It's Happening

- Baidu Inc. is unlocking significant hidden value through the planned spin-off and Hong Kong listing of its AI chip subsidiary Kunlunxin, announced in early January 2026. This move highlights the standalone potential of its proprietary semiconductor capabilities, with analysts estimating Kunlunxin could reach substantial valuations and drive focused growth in China’s domestic AI ecosystem, especially as geopolitical factors accelerate homegrown chip development.

- ERNIE 5.0 and multimodal AI advancements position Baidu at the forefront of China’s generative AI race. Launched in late 2025 with native omni-modal capabilities for text, images, audio, and video, ERNIE 5.0 delivers enhanced reasoning, tool use, and creative output, while upcoming Kunlunxin M100/M300 chips (rolling out in 2026-2027) power trillion-parameter training and large-scale inference—solidifying Baidu’s role in building a self-reliant AI infrastructure amid surging demand from enterprises and developers.

- Strong core search and AI Cloud momentum provides Baidu with a resilient revenue foundation. As China’s leading search engine with integrated AI features, Baidu continues to monetize traffic effectively, while its Qianfan cloud platform sees accelerating adoption for generative AI workloads, benefiting from national initiatives like “East Data, West Computing” that drive steady state-backed contracts and long-term growth in a high-priority sector.

- Apollo Go robotaxi expansion taps into the future of autonomous mobility. With over 10 million cumulative rides in China by early 2026 and international trials underway in markets like Switzerland and Turkey, Apollo Go’s sixth-generation RT6 vehicles are nearing unit-economic break-even in select cities, creating a high-margin, scalable narrative for Baidu in the emerging global autonomous driving market.

- Analyst Ratings:

- Freedom Capital Markets: Buy

- Jeffries: Buy

- JP Morgan: Overweight

My Action Plan (87% Return Potential)

- I am bullish on BIDU above $125.00-$126.00. My upside target is $280.00-$290.00.

Market-Moving Catalysts for the Week Ahead

The Delusion of Fed Independence

A new macroeconomic era is upon us. In reality, it's been in effect for a couple of years now, and it's one of fiscal dominance. Over the next couple years, I think that the idea of an independent Fed is going to slowly wither away.

Despite inflationary data staying tamed, the Fed is playing hardball with additional rate cuts. As a result, I wouldn't be surprised if the Trump administration "let" stocks correct in the coming months in order to entice the Fed into action.

Then, of course, there is the new lawsuit against Fed Chair Powell. It's too early to make judgements about the situation, but one cannot help but think this is a way of trying to get the Fed to move. Keep in mind Powell's term is up in just a few months.

Earnings Season is Underway

With the S&P 500 trading at elevated valuations after 2025's gains, investors are heavily reliant on sustained corporate profit growth to justify these levels and extend the rally. Consensus expectations point to solid ~8.3% year-over-year EPS growth for Q4, building on a full-year 2025 rise of around 12-13%.

Forward guidance for 2026 projects even stronger acceleration to 14-15%+ earnings expansion—fueled by AI-driven productivity, resilient consumer spending, rebounding dealmaking in financials, and potential policy tailwinds like deregulation.

Mixed early bank results (e.g., JPMorgan’s revenue beat but profit miss, alongside stronger showings from peers) and sector divergences (tech and financials outperforming, consumer discretionary lagging) have already introduced volatility, but upbeat 2026 outlooks—especially from AI beneficiaries and banks—could catalyze further upside and broaden participation.

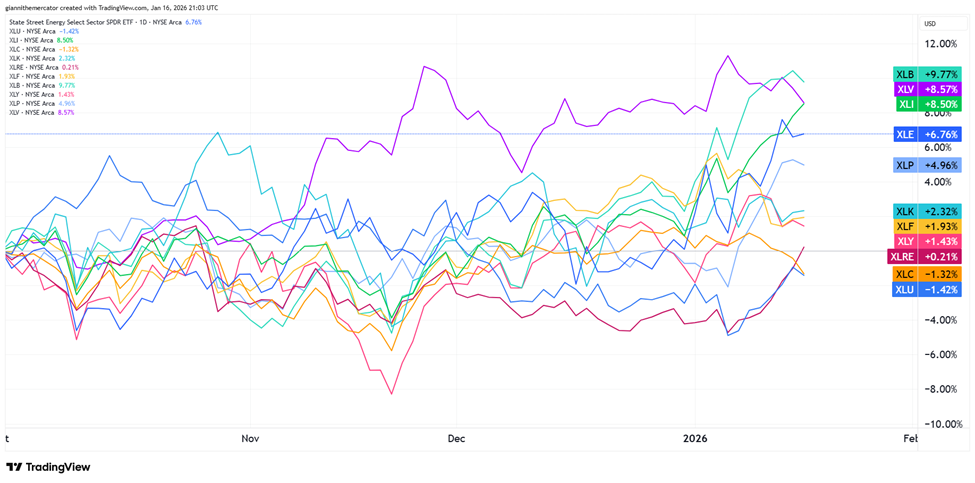

Sector & Industry Strength

A big shift just took place at a sector-based level. Healthcare (XLV) is no longer the top-performing sector since the start of the fourth quarter. It's been overtaken by basic materials (XLB), which marks a major regime shift.

In fact, industrials (XLI) are close to overtaking healthcare too. Even energy (XLE) has enjoyed a nice run in recent weeks. Utilities (XLU) are now the worst-performing sector since the start of the fourth quarter.

Meanwhile, the major indices are still stuck in congestion. This has to do with the tech sector (XLK) lagging for the past few months. Let's see if earnings season can get this sector back moving in the right direction.

| 1 week | 3 Weeks | 13 Weeks | 26 Weeks |

| Real Estate | Energy | Energy | Healthcare |

Editor's Note: This type of leadership tells us the rally is maturing.

A Critical Level for Metals (Sector ETF: GLD/SPY)

The rally in precious metals have completely blown away the expectations of everyone except the gold bugs. However, the outperformance from metals, and especially gold, is reaching a very key inflection point.

The chart below shows the ratio between gold (GLD) and the S&P 500 (SPY). Gold's outperformance against the S&P actually started back in late-2021, but it really began to accelerate back in the summer of 2024.

Now we're seeing the ratio take out the high from 2020. The big question now is whether we see a double top and some consolidation under resistance of the saucer formation, or whether we blow right through it and gold continues to go parabolic. If you haven't booked any gains in metal-related positions yet, it's time to do so.

Are Commodities Reawakening from Their Slumber? (Sector ETF: DBC/SPY)

I've been sharing this ratio periodically over the years. It's one of the most important ones, not only for gauging the state of inflation, but also it's general momentum. The chart below shows a basket of commodities (DBC) against the S&P 500 (SPY).

The ratio has been in a clear downtrend for years. Actually, it peaked in conjunction with the inflation data back in June 2022. It's been dropping cleanly within the descending price channel, signaling that stocks were the better trade over commodities.

But that could be on the verge of changing. The ratio is starting to break above the upper trendline of the channel. At the very least, this signals that the rate of descent is no longer in effect. Stocks may continue outperforming commodities, but by not as wide of a margin. This is step one before commodities eventually outperform again.

Junk Spread Tension (Sector ETF: HYG/IEI)

A big battle is taking place in the bond market, and it's happening between junk bonds (HYG) and 3-7 Year Treasuries (IEI). The ratio between these two segments of the bond market is displayed below.

In a healthy market environment, this ratio steadily climbs higher. The reason is because investors have a greater appetite for risk and junk debt is obviously riskier than Treasuries. Since last April, this ratio has been rising, but it's been losing momentum as of late.

If this ratio starts breaking lower, and Treasuries start outperforming junk debt, look for some volatility to creep into the equity market. Junk bonds have a tendency to trade similar to stocks when it comes to volatility, and as the saying goes, "Credit leads."

Cryptocurrency

This week, I want to turn our attention to Solana. Similar to Bitcoin and Ethereum, it's been in a corrective downtrend since the fall. However, this past week, prices took out the high of December 4, which is the first real instance of a higher-high in months.

This is the first signal that the strength of the downtrend is weakening. There's also a rounding bottom formation on this chart, and if prices break out above the upper horizontal trendline acting as resistance, a surge up to the 170.00-175.00 level could follow.

Note how 170.00-175.00 is just under the key resistance zone that was formerly support at 175.00-190.00. If prices were to clear that level, it would confirm that the bear market is over and a new bull trend is underway. In time, I can see Solana being a 500.00 coin.

Legal Disclosures:

This communication is provided for information purposes only.

This communication has been prepared based upon information, including market prices, data and other information, from sources believed to be reliable, but Benzinga does not warrant its completeness or accuracy except with respect to any disclosures relative to Benzinga and/or its affiliates and an analyst’s involvement with any company (or security, other financial product or other asset class) that may be the subject of this communication. Any opinions and estimates constitute our judgment as of the date of this material and are subject to change without notice. Past performance is not indicative of future results. This communication is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Benzinga does not provide individually tailored investment advice. Any opinions and recommendations herein do not take into account individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. You must make your own independent decisions regarding any securities, financial instruments or strategies mentioned or related to the information herein. Periodic updates may be provided on companies, issuers or industries based on specific developments or announcements, market conditions or any other publicly available information. However, Benzinga may be restricted from updating information contained in this communication for regulatory or other reasons. Clients should contact analysts and execute transactions through a Benzinga subsidiary or affiliate in their home jurisdiction unless governing law permits otherwise.

This communication may not be redistributed or retransmitted, in whole or in part, or in any form or manner, without the express written consent of Benzinga. Any unauthorized use or disclosure is prohibited. Receipt and review of this information constitutes your agreement not to redistribute or retransmit the contents and information contained in this communication without first obtaining express permission from an authorized officer of Benzinga. Copyright 2022 Benzinga. All rights reserved.